[ad_1]

Anyone can open a 529 College Savings Account, but most people don’t.

Surveys have consistently shown that a large portion of Americans are unaware of the accounts and their purpose. Here’s what you need to know:

What is a 529 account?

This is a college savings account similar to what 401 (k) accounts are for retirement. You contribute to the account. Then these contributions are invested so that the account generates more money. This money grows tax-free and can later be used for college or vocational school.

The name “529†comes from the section of the Internal Revenue Code that describes the tax policy governing these accounts.

RELATED: Can you change a child’s life with $ 25? Fund My Future Milwaukee thinks so.

Why use this plan instead of a regular savings account?

These 529 savings accounts help you ensure that the value of your money grows with the market. If you put a dollar in a savings account, 20 years from now that dollar won’t go that far because of inflation, since the costs of goods and services increase over the years.

Savings accounts have very low interest rates, which are usually much lower than the returns on investments. The 529 accounts offer more growth potential. The market fluctuates, but the idea is to create an account early – again similar to a 401 (k) – so the account can absorb those ups and downs while still making income.

What can the money be used for?

A lot.

The funds can be used for tuition, room and board, books and other equipment at universities, colleges, trade schools and technical schools – any post-secondary education opportunity eligible for a federal loan ( which means the federal government does not view it as a risky investment).

Who can use the money in the account?

A parent or guardian usually opens the account for their child, who is called the “beneficiary” of the account. The money can be used by the child.

But if the child chooses not to pursue any post-secondary training or education, the account can be used for educational purposes by a sibling, parent or other immediate relative without any penalty.

The account holder can withdraw funds himself for non-educational purposes, but will have to pay taxes on the money earned.

When should I start saving?

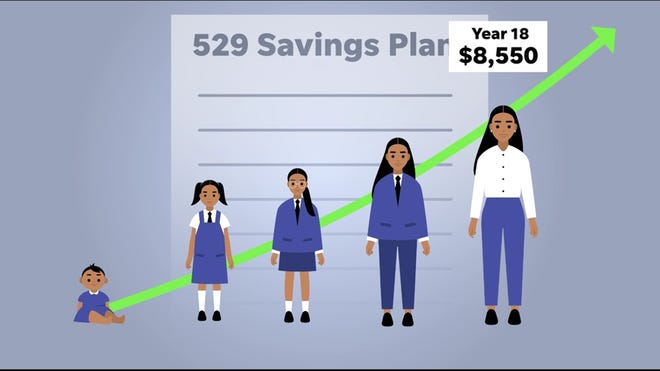

Right now.

The earlier you start the account, the more time your investment has to grow. It can help small amounts turn into thousands of dollars.

For example, if you open an account with $ 25 and contribute $ 5 per week for 18 years, you will have about $ 8,550 to use for college or other training programs – almost twice as much as you would if you put that amount in a regular savings account.

What are the advantages of this account?

There are financial benefits and Wisconsin offers tax breaks for residents who contribute to 529 education savings plans.

Research has also shown that having an account, regardless of the amount invested, makes it more likely that a child will go to college.

One study found that among children who plan to go to college, those who have a savings account are six times more likely to go than those who don’t.

Having a savings account was a better predictor of whether a child with those expectations would go to college than the parents’ race or net worth, the study showed.

Will it hurt a student’s financial aid?

If a parent or guardian opens an account, it usually has less of an impact on a child’s eligibility for university financial aid, as it is not counted as the student’s income, especially relative to to other savings mechanisms.

A 529 account can also be opened by a grandparent, another parent, or an individual, but in these cases, it is more likely to affect the child’s eligibility for financial aid.

It doesn’t matter who opens the account, anyone can contribute, even if they are not a parent or the person who opened it. A student can also be named beneficiary of multiple accounts.

When can we access it?

The money is technically accessible at all times, but if you use it for non-educational purposes, you will have to pay taxes on the money earned.

The plans allow up to $ 10,000 per year to be used for private tuition fees for Kindergarten to Grade 12. You can also use the money in the account to make a one-time student debt payment of up to $ 10,000.

In general, the goal is to save for when a child enters college or other training programs after high school.

What types of accounts are available in Wisconsin?

Wisconsin has two 529 college savings platforms.

Edvest requires an initial deposit of $ 25 and can be set up online without the assistance of a financial advisor. This is the platform used by Fund my future Milwaukee, which has a long-term goal of opening a 529 account for every 5-year-old kindergarten child in the city.

Edvest got a bronze rating last year, ranking it among the best plans in the country, according to a analysis by investment research firm Morningstar Inc.

Tomorrow’s Scholar is an advisor-sold plan, which means it’s accessible through a financial planner. It requires an initial deposit of $ 250.

Tomorrow’s Scholar received a negative rating from Morningstar. It was one of eight plans that “charge a fee that investors are better off avoiding,” the research firm reported.

Should I use a Wisconsin plan?

No.

Other states have 529 plans that might better meet your family’s needs.

How does the investment work?

If you open an account with Edvest yourself, you can choose different levels of investment risk.

The most popular option is a “targeted enrollment†investment, in which your account takes slightly riskier investments early, and then makes more cautious investments as college time approaches for your business. child. This is to ensure that your account balance does not fluctuate too much as your child needs it.

Are there any fees?

Edvest of Wisconsin does not have a monthly or annual fee to keep the account open.

He has asset-based fees depending on the underlying investment funds and these are paid indirectly which means you don’t get a bill that you have to pay.

If you withdraw money from a 529 plan for expenses that don’t qualify under the education guidelines, you may face penalty charges. With Edvest, you have to pay state and federal taxes, plus a surcharge 10% tax penalty on earned income, not on how much you contributed.

Is there a minimum balance required?

Other than the initial deposit, there is no minimum balance required in the Wisconsin Edvest plan.

What information do I need to open an account?

To open an Edvest account, you need:

- Your address and date of birth, as well as your social security number or tax identification number.

- The date of birth and the social security number of the child who will be the beneficiary of the account.

- Bank information (account and routing numbers) for the initial deposit. You can also send a check by mail.

Will opening this account disqualify me from public aid?

That could have an effect, said Linda Lambert, head of financial capabilities at the Wisconsin Department of Financial Institutions.

States may have different rules on asset limits – and a 529 plan is considered an asset – for public assistance programs.

In Wisconsin, for example, 529 plans are counted as an asset in determining whether someone is eligible for the state’s Temporary Assistance for Needy Families program, Wisconsin Works (W-2).

What if I am undocumented but my child is a U.S. citizen?

At present, the account holder must have a social security number.

Edvest is pursuing an option that would allow an undocumented parent to gain access to their child’s account, although he is still not the owner of the account, according to Lambert.

“So even though it’s not available today, it probably will be in the future,†she said.

If I use a Wisconsin plan, can my child attend school only in Wisconsin?

No.

The Wisconsin plans can be used for post-secondary education opportunities across the country that are eligible for a federal loan.

You have more questions ?

Edvest offers a variety of webinars and Resources. Other 529 plans offer guides and services. Financial advisers can also answer questions about 529 plans and if they are the best tool for your savings goals.

Contact Ashley Luthern at [email protected]. Follow her on Twitter at @aluthern.

[ad_2]