JHVEPhoto

easy (TSX:GSY:CA) (OTCPK:EHMEF) Canada’s largest venture lender has been an incredible stock to own for the past 5 years. The company has found the middle ground between the riskier payday loan market and the main big bank lenders. The Company’s core segment, easyfinancial, is a network of stores offering personal, home and auto loans. This has been the company’s focus for the past 8 years as its easyhome rental segment has mostly flat revenue/profits. Recently, the company has entered the booming online point-of-sale and lending business to support growth. Strong growth in the loan portfolio, smart equity investments and good management led to a significant outperformance of equity appreciation during this period. It has been one of the best performing stocks on the Toronto Stock Exchange for the past 10 years. The company has a strong dividend yield of 2.54% and has been growing every year for many years, making it extremely attractive to investors. The nature of its business in high-risk subprime lending kept some institutions on the sidelines, but that turned out to be a mistake as the company fired full steam ahead. The company recently reported a very strong second quarter impression even as recession fears ripple through the markets.

Q2 Print offers long-term confidence

goeasy tends to have a very stable quarter-over-quarter performance for a small-cap stock, with consistent growth in revenue and profitability over the past few years. Revenue growth was 24.4% over the prior year to CAD 252 million. The key metric moving the stock on a shorter-term basis is loan creation — new loans the company created during the quarter. The second quarter was a huge quarter for loan applications with the highest number of applications ever for the company. The company recorded an extremely strong $628 million in originations in the quarter, with loan growth of $216 million after taking into account runaway loans. After the quarter, the company holds loans of C$2.37 billion, showing how strong originations are today. Some of this strength is due to company-specific factors such as the new auto loan product, which management announced as it was $50 million in the quarter, up 450% from compared to last year. They also saw home equity lending strength up 169% from a year ago. These home equity loans are secured against the value of the home, reducing the risk for GSY. This is one of the factors that has enabled goeasy to reduce its net charge rate from 13% a few years ago to a range of 9-10% today. That means a smaller loan loss provision is needed, and more money for the bottom line with a record operating profit of $85 million or an operating margin of 35.3%. The downside of a lower yield on these higher performing loans is negated by the increased credit quality and stability they provide to the business over the long term.

Another factor in the strength of subprime consumer lending is recent inflation issues weighing on low-end consumers. This means that more people may need to take out a loan to consolidate debt or meet large payment obligations. GSY mentioned how strong the demand for motorsports and home improvement was, detracting from the impending recession theory discussed recently. These are discretionary purchases for which someone who has gone bankrupt may have to turn to GSY if they cannot lend from the major Canadian banks. The company also noted on the second quarter conference call that the lending requirements of the Big 5 Canadian banks have tightened, causing some low-end customers to pull out of the big banks. The record number of customers this quarter seems to suggest that this is a factor at play. This tailwind should help going forward, as inflation is unlikely to subside soon and spending remains probably tight at the lower end of the income scale where GSY has customers.

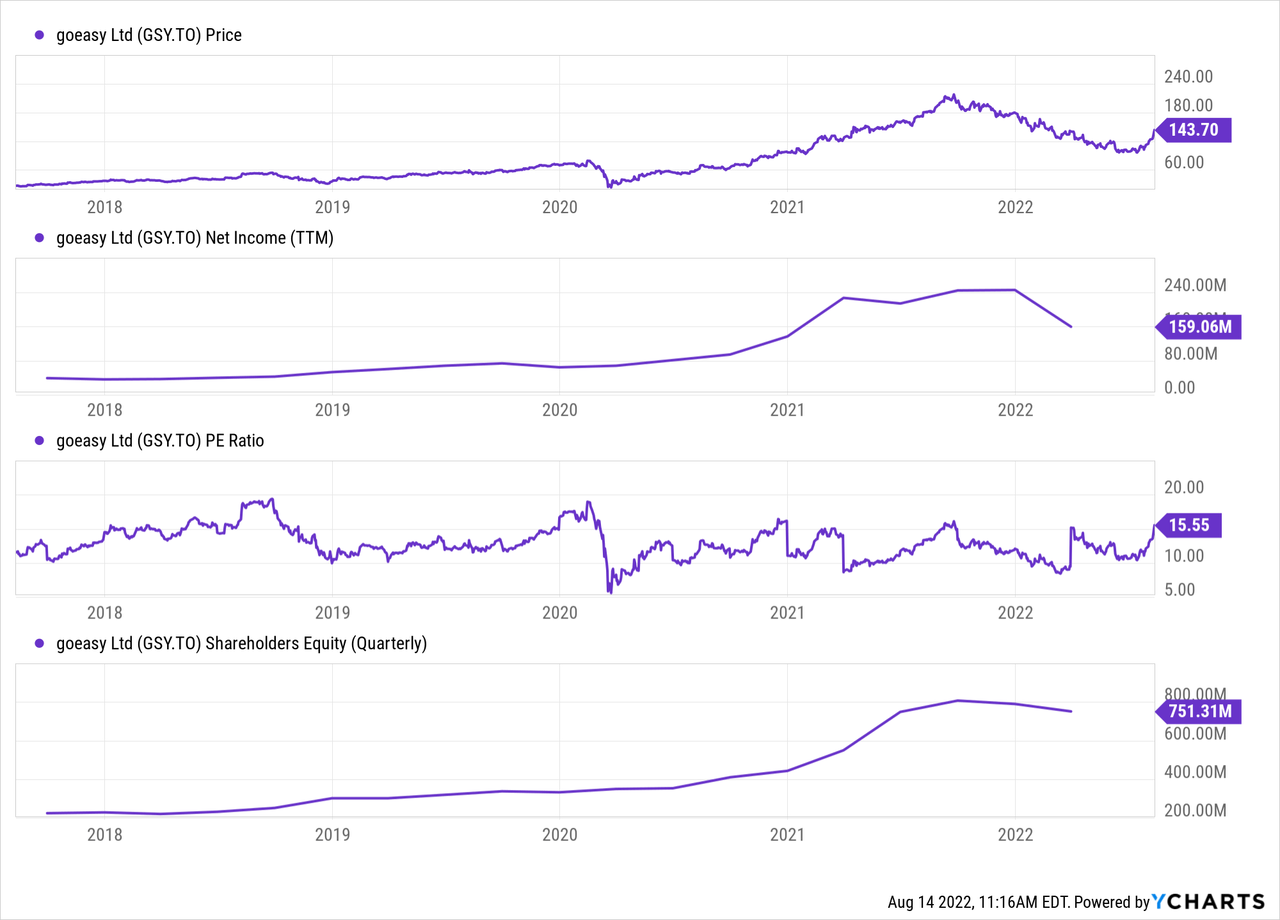

As you can see above, the business is actually cheaper on a price to earnings basis than it was before Covid-19 in late 2019 and mid 2018. However, the business still benefits a lower impaired loan rate and a higher growth rate. The stock’s fair value is likely in the high $100 range with a solid 10-20% share every year with strong performance. Keep in mind that because the company has a strong background, GAAP net income is reduced in the short term by an increase in loan loss provisions, with this income being built up in future quarters as the loans are repaid. You can see it in the chart above with TTM’s net profit shrinking to $159 million. Yet the company is trading at just 15x the lagging P/E, just a little higher than the 5-year average. The company plans to nearly double its loan portfolio by the end of 2024 to around C$4 billion, which would mean significant growth still to come. That’s with a moderate addition of 20-35 locations over the next two and a half years, showing that it’s mostly coming from the efficiency of their current locations. This helps increase the company’s operating margin, even with a 2% lower yield on consumer loans. The increased advantage of its online lending offerings helps increase operating margin over time as the business benefits from scale.

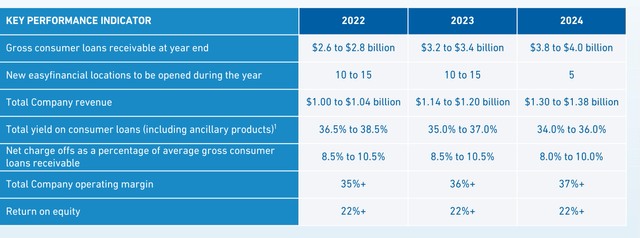

Performance indicators (GSY Q2 presentation)

Canada boosts investment

goeasy made a significant acquisition last year with its purchase of LendCare to give itself a strong footing in the auto lending and powersports space. They paid $320 million for the business, acquiring $404 million in loans to support growth. LendCare has been a major asset to them over the past year with a mostly secure wallet, with a lower interest rate helping to reduce charges and bad debts. This area has provided a new vertical for goeasy to lend to, helping to propel the next stage of growth while improving credit quality. They have just invested C$40 million in Canada Drives, the largest online car buying and delivery platform in Canada. Non-preferred customers of Canada Drives will be able to obtain loans through GSY, contributing to growth in this area. Over 100,000 customers have been referred from Canada Drives over time, and the strengthening of this partnership is a significant benefit. GSY has also had great success in similar investments in the past, with a $34.3 million investment in Paybright in September 2019 that turned into a huge gain in Affirm (AFRM) shares upon its acquisition. The gain on this purchase to date is 3.2 times the initial investment, an impressive gain of C$109 million as of August 2022. These smart moves help provide confidence that the company will be able maintain revenue and earnings growth of more than 15% even as the loan portfolio becomes less risky.

Risk factors

The market views risks such as a possible bill to lower the legal interest rate in Canada as unlikely. Bills like this have been introduced in the House of Commons of Canada in the past, but have never been successful enough to move forward to a vote. The reason being, as CEO Jason Mullins has argued, it actually pushes consumers into things like payday loans that don’t help rebuild credit. To hedge against this unlikely possibility, the company has reduced its blended interest rate, with the growing use of secured loans offsetting this potential risk to some extent.

The risks of recession due to the subprime consumer were largely denied during the Covid-19 pandemic. Many customers try to rebuild their credit ratings and thus take out loan protection that prevents write-offs during bad economic times. Additionally, many customers with unsecured loans do not own their own homes, which means less difficulty repaying the loans than those who find themselves struggling with a mortgage. This remains the biggest risk for the stock, with the stock showing some volatility during the March 2020 Covid-19 shock. The stock fell from $79 to a low of $20 with no deterioration in fundamentals. Keep in mind that similar shocks are a risk in the future, as thinly traded small cap stocks with perceived risk during the recession.

Conclusion – An essential Canadian action

The reward for goeasy has far outweighed the risk over the past few years and the company has significantly reduced its risk profile over time. Some avoid the stock because of its perception as a “sinful” stock or that it will crash in a recession. However, these unfounded fears simply mean increased shareholder returns for those who invest. The company is strong with a growing online presence, improved brand image and impressive ROI. I highly recommend US investors take a look at this name, as it trades over-the-counter under the ticker symbol EHMEF. Keep in mind that if you are buying in USD liquidity and volume will be quite low and use limit orders to average the name. It has far outperformed its US peers in the space, with lower-end Canadian consumers exhibiting a higher risk/reward profile. The company will continue to grow in the years to come, with more dividends, making it a very attractive financial value for any portfolio.