[ad_1]

It’s no secret that Square, Inc. (NYSE: SQ) has done very well lately, outperforming its peers and the broader market. Although the business continues to grow, it faces challenges from current and new competitors.

In this article, we’ll take a look at Return on Equity (ROE) and see where it stands relative to the current valuation.

See our latest analysis for Square

Trying to stay one step ahead

Amazon is allegedly worked on a new point of sale (POS) system which may be old for third party sellers. This system will handle both online and offline transactions and integrate with services such as Prime and Flex. Although the company is silent on the project so far, it will allow it to compete with established players like Square, Shopify (NYSE: SHOP) or PayPal (NASDAQ: PYPL).

Meanwhile, Carré Just announced that sellers would be able to accept payment via Cash App Pay. This will allow a new contactless payment method for online and in-person transactions, as customers will scan the seller’s QR code at checkout. This option adds variety for over 70 million active customers and further reduces withdrawal frictions.

Hedgeye, a research platform known for its entertaining comics related to the marketSquare added as a prominent bullish idea – citing the business model suited to the current macroeconomic environment, the disruptive potential and a proven track record of successful execution.

Define the ROE

Return on equity or ROE is a test of how effectively a company increases its value and manages investor money.

In other words, it is a profitability ratio that measures the rate of return on capital contributed by the shareholders of the company.

How is the ROE calculated?

Return on equity = Net income (from continuing operations) ÷ Equity

So, based on the above formula, Square’s ROE is:

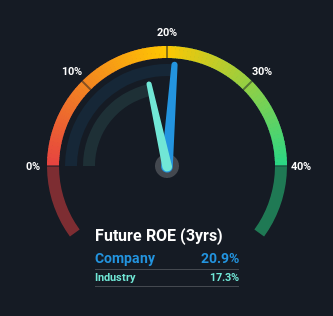

21% = US $ 573 million ÷ US $ 2.7 billion (based on the last twelve months to June 2021).

The “return” is the profit of the last twelve months. So this means that for every $ 1 invested by its shareholder, the company generates a profit of $ 0.21.

Does Square have a good ROE?

By comparing a company’s ROE with its industry average, we can quickly measure how good it is. It is important to note that this measure is far from perfect, as companies differ considerably within a single industry classification.

As you can see in the graph below, Square has a higher ROE than the IT industry average (17%).

This is what we love to see. However, keep in mind that a high ROE does not necessarily indicate efficient profit generation. Besides changes in net income, high ROE can also be the result of high leverage to equity, which indicates risk.

You can see the 4 risks we have identified for Square by visiting our risk dashboard for free on our platform.

The importance of debt to return on equity

Most businesses need money (from somewhere) to increase their profits. This liquidity can come from the issuance of shares, retained earnings or debt.

In the first two cases, the ROE will capture this use of capital to grow. In the latter case, the debt used for growth will improve returns but will not affect total equity. Thus, recourse to debt can improve ROE, but with additional risk in the event of turbulence.

Combine Square’s debt and its 21% return on equity

Of note is Square’s high reliance on debt, leading to its debt-to-equity ratio of 2.07. While its ROE is respectable, it should be borne in mind that there is usually a limit to the amount of debt a business can use.

Debt brings additional risk, so it’s only really worth it when a business is making decent returns.

Conclusion

Return on equity is a useful indicator of a company’s ability to generate profits and return them to shareholders. In our books, the highest quality companies have a high return on equity, despite the low leverage.

For example, PayPal (NASDAQ: PYPL) has a slightly higher ROE (23.3%) while simultaneously having a lower debt ratio. You can see more details on our platform. Meanwhile, Shopify (NYSE: SHOP) has a 24.2% ROE and a tiny debt-to-equity ratio.

But ROE is only one piece of a bigger puzzle, as high-quality companies often trade at high earnings multiples. The growth rates of earnings relative to expectations reflected in the stock price are essential to consider.

So maybe it’s worth checking this out free analyst forecast report for the company.

If you would rather consult another company with potentially superior finances, don’t miss this free list of interesting companies with HIGH return on equity and low leverage.

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no positions in any of the companies mentioned. This article is general in nature. It does not constitute a recommendation to buy or sell shares and does not take into account your goals or your financial situation. Our aim is to bring you long-term, targeted analysis based on fundamental data. Note that our analysis may not take into account the latest announcements from price sensitive companies or qualitative documents.

Do you have any feedback on this item? Are you worried about the content? Contact us directly. You can also send an email to [email protected]

[ad_2]